“I haven’t found a product out there that delivers the same way The Mortgage Office does. Some might have a bell or whistle here and there, but at the end of the day they’…

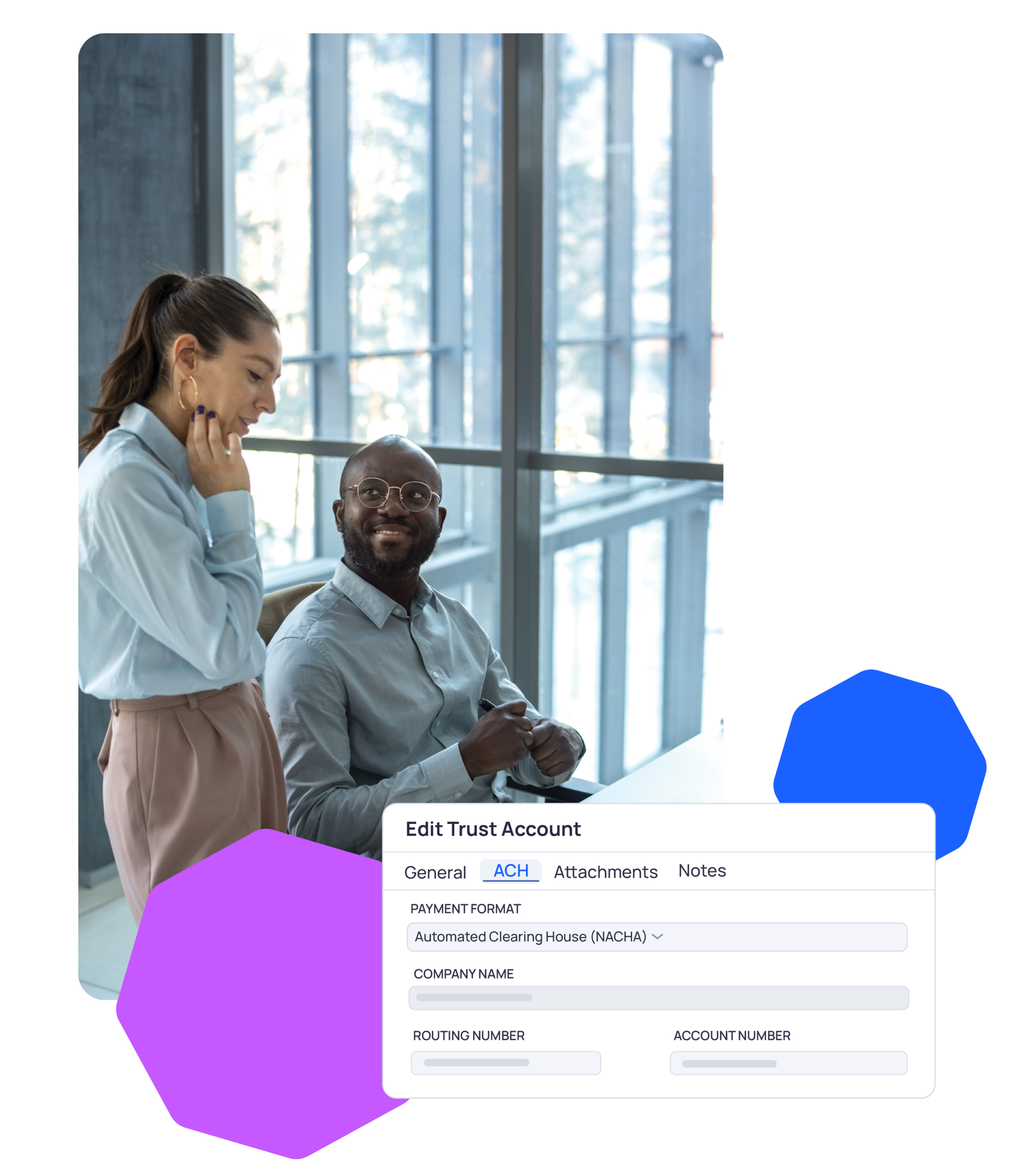

Electronic Funds Transfer (EFT’s)

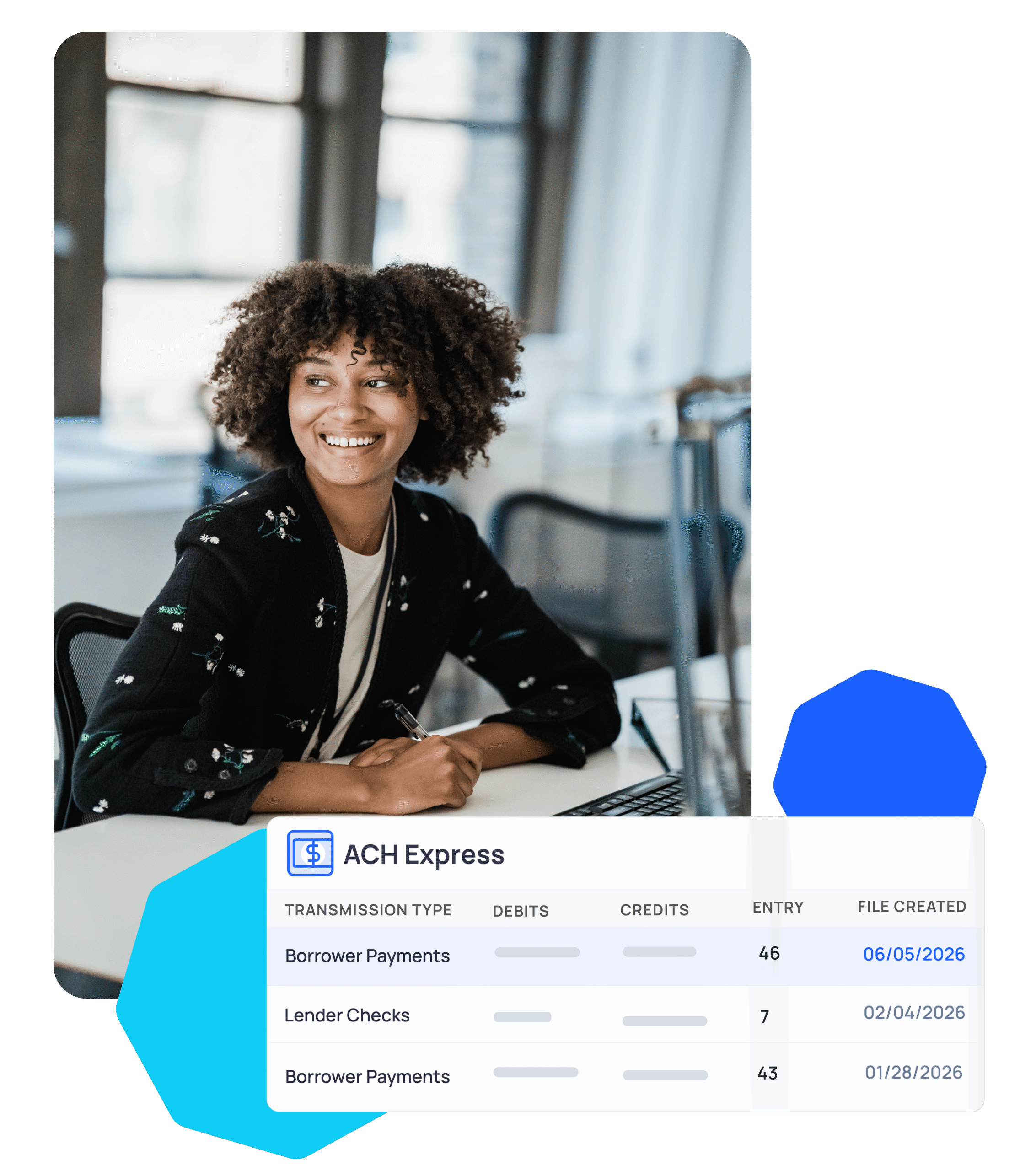

Apply Payments And Send Remittances In Clicks

Collect borrower payments and pay lenders and vendors faster, with support for multiple payment rails across the US, Canada, Australia, and New Zealand.

JUMP TO:

SEE THE DIFFERENCE

Automate Critical Payment Actions

From scheduled borrower payments to lender remittances, EFT automates the routine touchpoints in your servicing workflow, freeing your team to focus on higher-value work.

- EFT formats supported across the US (ACH), Canada, Australia, and New Zealand

- Reliable bulk application for every borrower payment

- Additionally, import CSV lockbox files for bulk payment application from third party processors

Solutions & Capabilities

Send and receive payments in clicks, not hours.

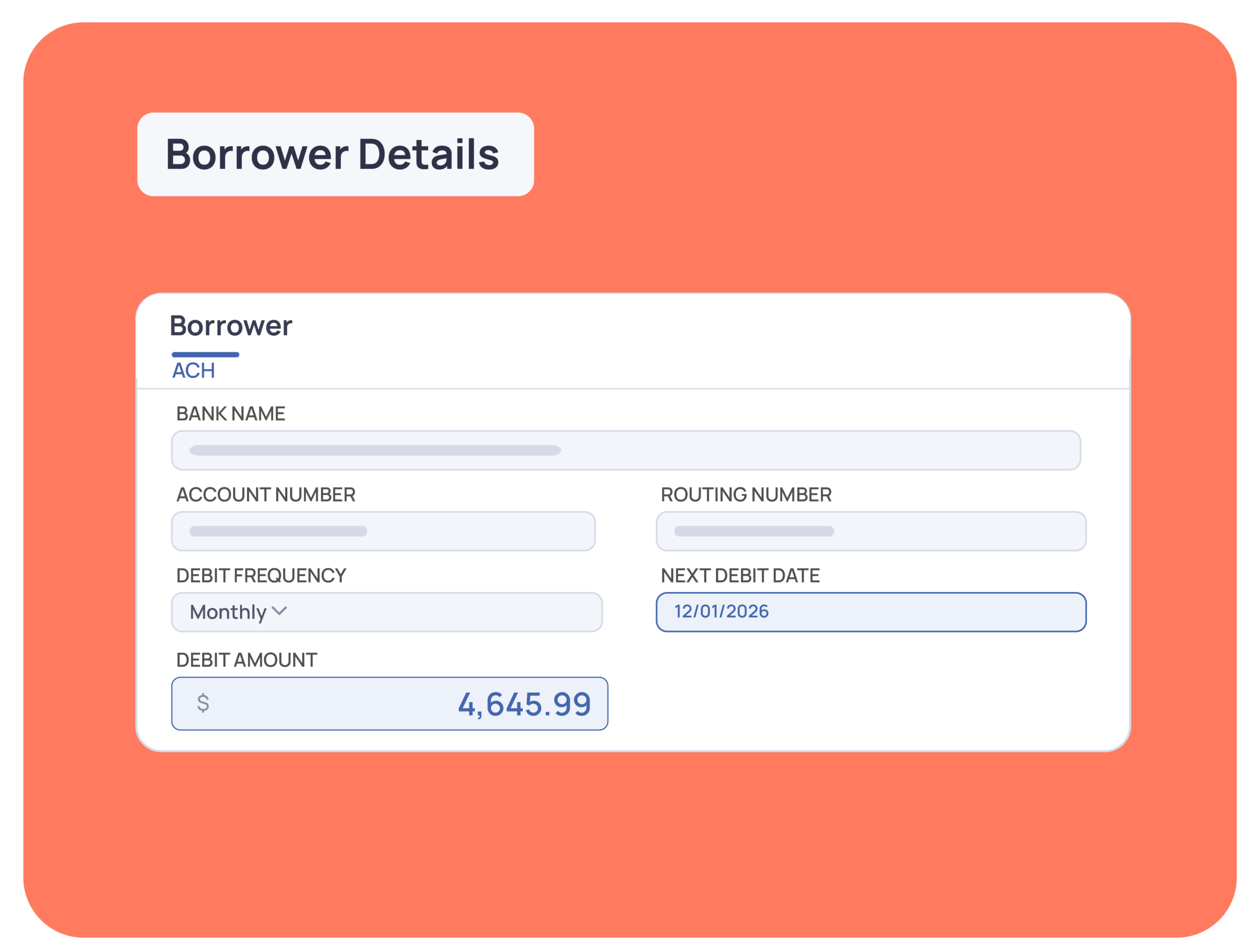

Borrower Payment Application

When checks are ready to be sent to Lenders for their principal and/or interest payments, issue payments without delays.

- Filterable options so that you can apply payments across varying slices of the servicing portfolio

- Automation advances next payment dates after each payment in alignment with the payment frequency

- Payment history reflects which payments were applied via EFT, with granular payment distribution retained

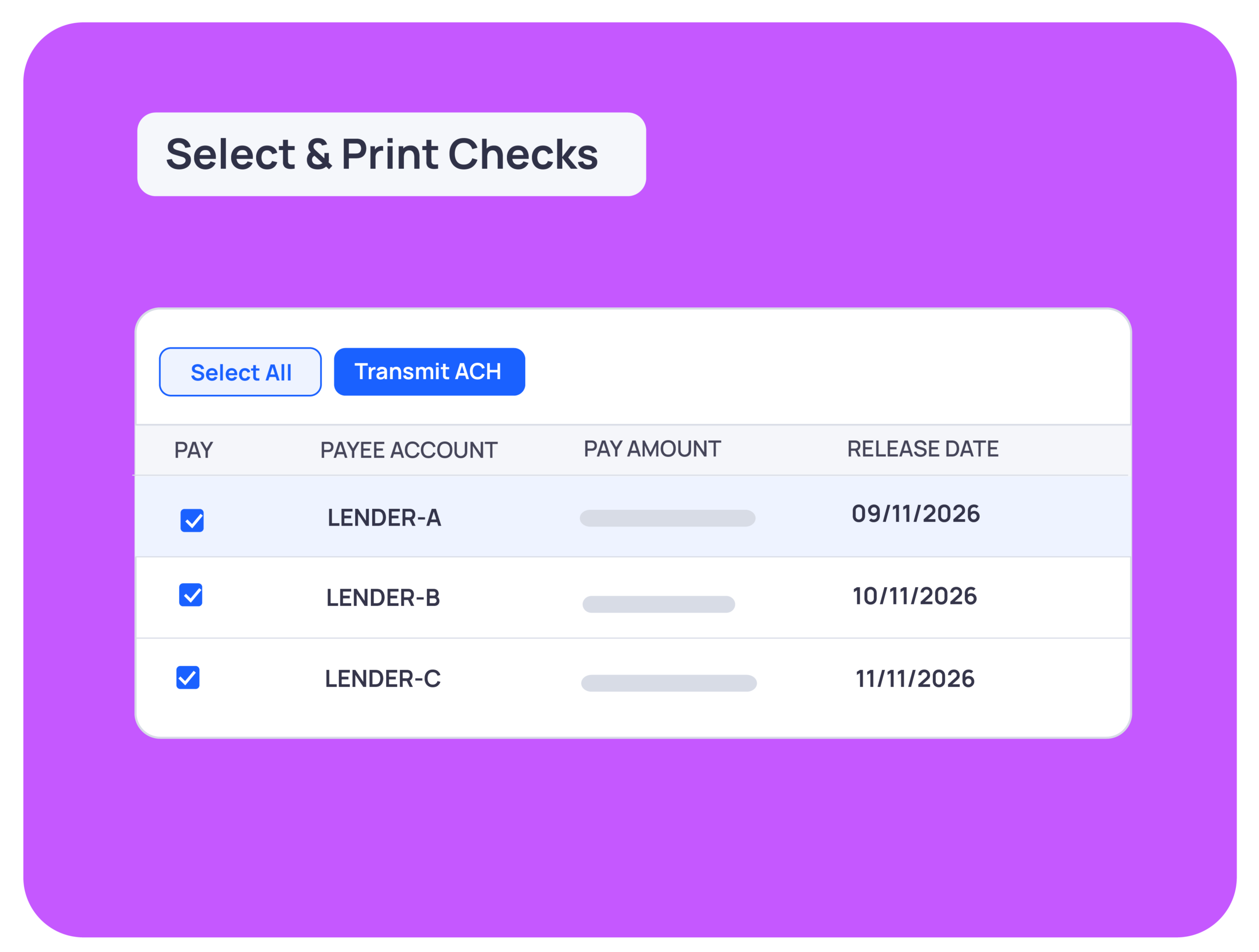

Timely Lender Remittances

When checks are ready to be sent to Lenders for their principal and/or interest payments, issue payments without delays.

- Aggregated reporting supports reviews for any Lender check activity

- Retain Lender bank details on their respective profile for use with each payment

- Send Notification of Electronic Deposits for each lender in a few clicks

Consistent Vendor Payments

Seamlessly send third-party vendor payments for a more efficient payment solution to irregular payments.

- When issuing payments to Insurance, Taxes, Contractors, and more, disburse these funds without delay

- Integrates directly with issuing Vendor vouchers and disbursements

- Statements and account history reflect which payments were issued via EFT

HOW IT WORKS

From Setup to Disbursement

Step 1

Add EFT Details

Add any Borrowers, Lenders, and Vendors to TMO, and configure each with their respective banking details.

Step 2

Capture Borrower Payments

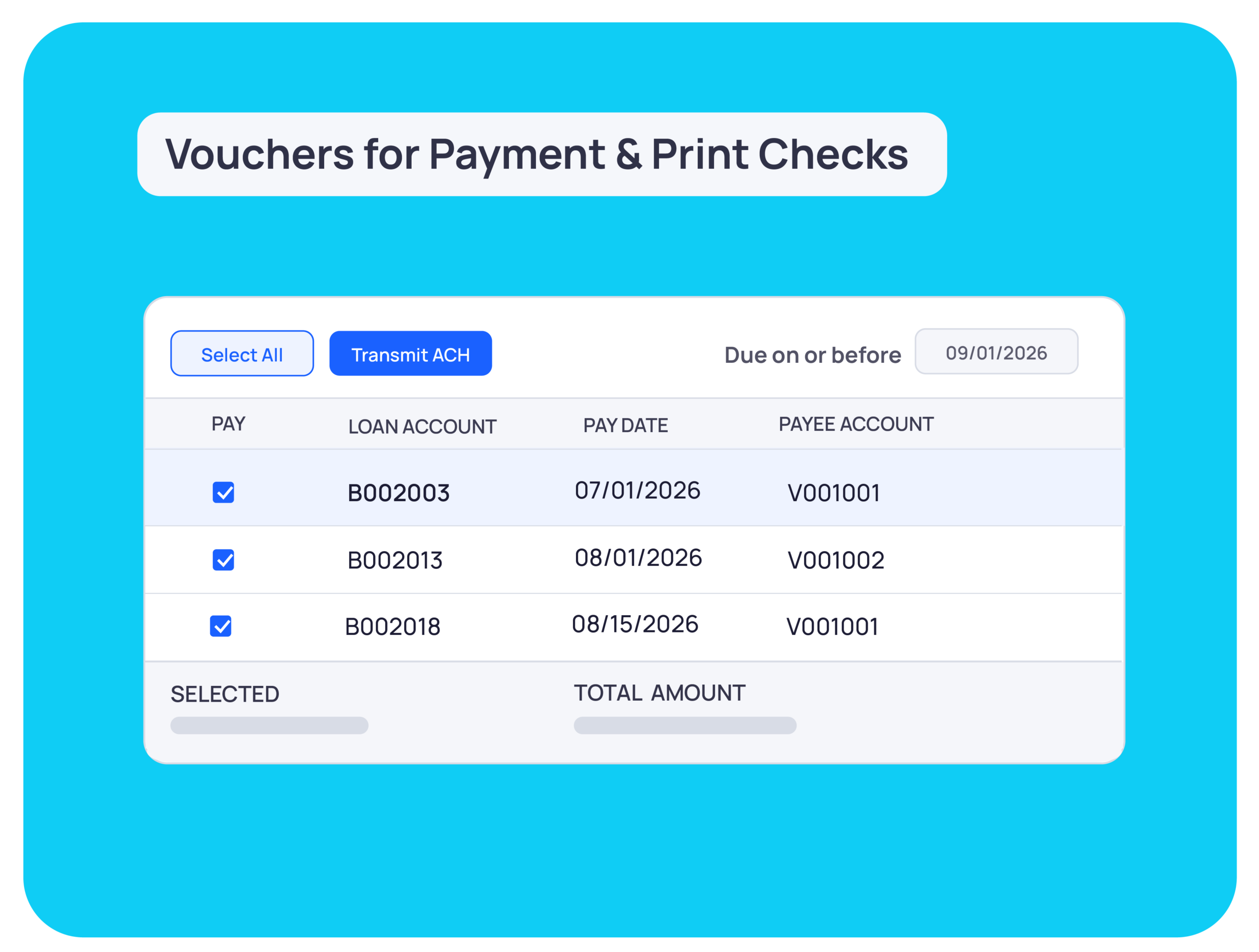

Executing a billing run will cross reference regular payment details across eligible Borrowers to generate record of all payments.

Step 3

Moving Monies

Transmit or manually upload the relevant banking file to your financial institution to process payments.

Step 4

Issuing out Remittances or Disbursements

Open Lender payments, Vendor disbursements, Investor distributions, or Construction draws, and issue their respective payments in minutes.

See ACH payment processing in action

SECURITy & Compliance

Compliance is a priority at every step in the process.

Implement a more efficient payment solution without compromising the security or quality necessary when processing these payments.

- Retain these critical banking details with TMO’s secure encryption.

- Utilize granular controls to determine those who have access to apply and send payments.

- User events are logged with each payment action directly on the relevant profile for historical visibility and audits.

Partnerships & Integrations

Connect EFT payment processing and our robust servicing platform with your team’s existing tools and other powerful integrations to keep payment data accurate, reduce manual work, and strengthen reporting as you scale.

FAQs

What banking formats are supported for accepting and sending payments?

Support is currently available for the following formats.

- Automated Clearing House (NACHA) United States

- Australian Payments Clearing Association (BECS) Australia

- Canadian Payments Association (CPA 1464) Canada

- HSBC Bank Canada (CPA 1464) Canada

- CIBC Bank Canada (CPA 1464) Canada

- RBC Bank Canada (CPA 1464) Canada

- TD Commercial Banking (CPA 1464) Canada

- TD Commercial Banking (EFT80) Canada

- Bank of Montreal (CPA 1464) Canada

- Scotia Bank (CPA 1464) Canada

- Bank of New Zealand (IB4B) New Zealand

What happens if a borrower’s pay has nonsufficient funds and needs to be marked as an NSF?

When informed that a payment was unsuccessful, individual payments are able to be reversed while automating the generation of an NSF notice.

What is an EFT payment in mortgage servicing?

An EFT (Electronic Funds Transfer) payment in mortgage servicing is any electronic movement of money between bank accounts, including ACH debits, to collect borrower payments or send lender and vendor remittances. ACH is the most common form of EFT in mortgage servicing, operating as a batch network for scheduled and recurring payments. The Mortgage Office supports EFT payment processing across the US, Canada, Australia, and New Zealand.

What is the difference between EFT and ACH in mortgage payments?

EFT is the broad umbrella term for any electronic movement of funds between bank accounts, while ACH (Automated Clearing House) is one specific payment rail that operates within that category. In mortgage servicing, ACH is the most widely used EFT method because it supports scheduled recurring debits, bulk payment runs, and lender remittances through a regulated banking network. Understanding this distinction matters when evaluating which payment formats your servicing software supports.

How does The Mortgage Office handle EFT payment setup for borrowers, lenders, and vendors?

In The Mortgage Office, EFT setup follows a four-step workflow: add borrowers, lenders, and vendors to the platform and configure each profile with their respective banking details, then execute a billing run to generate payment records, transmit or upload the banking file to your financial institution, and finally issue remittances or disbursements directly from the platform. Each profile, borrower, lender, or vendor, stores banking details securely with encryption for reuse across every payment cycle. This centralized setup eliminates the need to re-enter banking information for recurring transactions.

What steps does The Mortgage Office use to apply borrower payments via EFT?

The Mortgage Office applies borrower EFT payments through a configurable payment application workflow: a billing run cross-references regular payment details across eligible borrowers to generate a complete payment record, the resulting banking file is transmitted or manually uploaded to your financial institution, and payments are applied with filterable options so servicers can target specific slices of the portfolio. Automation advances each loan’s next payment date after application, and payment history records which transactions were processed via EFT with granular context. This eliminates manual per-loan posting and reduces misapplication risk across large portfolios.

How does The Mortgage Office support lender remittances through EFT?

The Mortgage Office stores each lender’s bank details directly on their profile and uses those details to issue principal and interest remittances electronically without delays. Aggregated reporting gives servicers a consolidated view of all lender check activity, and the platform sends a Notification of Electronic Deposit to each lender in a few clicks. This removes the manual check-cutting process and creates a documented, auditable remittance trail.

Can The Mortgage Office send EFT payments to third-party vendors like insurance companies and tax authorities?

Yes, The Mortgage Office supports EFT disbursements to third-party vendors including insurance carriers, tax authorities, contractors, and other payees directly from the platform. Vendor payments integrate with the voucher and disbursement workflow, and statements automatically reflect which payments were issued via EFT for clear recordkeeping. This eliminates manual check processing for routine vendor obligations and reduces disbursement delays.

What EFT payment formats and regions does The Mortgage Office support?

The Mortgage Office supports EFT payment formats across four regions: the United States, Canada, Australia, and New Zealand, covering the primary ACH and direct-entry banking file standards used in each market. In addition to native EFT processing, the platform accepts imported CSV lockbox files for bulk payment application from third-party processors.

How does The Mortgage Office prevent misapplication of EFT payments across a large loan portfolio?

The Mortgage Office prevents misapplication by configuring payment application rules at the database level with loan-level options, ensuring consistent logic is applied across every borrower payment in a billing run. Filterable options allow servicers to apply payments across specific segments of the portfolio, by loan type, status, or other criteria, rather than applying a blanket rule that may not fit every loan. Payment history records each transaction with granular context, creating a clear audit trail if a misapplication needs to be investigated.

How does The Mortgage Office protect sensitive banking data used for EFT transactions?

The Mortgage Office secures borrower, lender, and vendor banking details using encryption at rest, ensuring that routing numbers and account numbers stored on each profile are protected from unauthorized access. Granular user-permission controls determine which staff members can view, enter, or modify banking details and which can initiate or approve payment transmissions. Every payment action is logged as a user event directly on the relevant profile, creating a complete audit trail for compliance reviews.

How does importing a CSV lockbox file work for bulk EFT payment application in The Mortgage Office?

The Mortgage Office accepts CSV lockbox file imports from third-party payment processors, allowing servicers to bulk-apply borrower payments collected outside the platform’s native EFT workflow. The import maps payment records to the corresponding loans in the servicing database and applies them according to the same configured payment application rules used for direct EFT transactions. This is particularly useful for servicers who receive payments through external lockbox services but want a single system of record for all payment history.

How do I find out where an EFT payment came from or confirm it was applied correctly?

In The Mortgage Office, each EFT payment is recorded in the loan’s payment history with granular context indicating the payment method, amount, distribution, application date, and the user event that triggered it. Servicers can trace any EFT transaction back to the billing run or manual action that generated it, and lender remittances include aggregated reporting for a full view of check and deposit activity.

How does The Mortgage Office help servicers stay compliant when processing EFT payments?

The Mortgage Office addresses EFT compliance at every layer: banking details are encrypted, user access to payment functions is controlled by granular permissions, and every payment action is logged with a timestamp and user attribution directly on the relevant profile. This audit trail supports compliance with Regulation E requirements around authorized debits, Regulation X requirements for timely payment crediting, and investor reporting obligations for payment reversals and no-pay scenarios. Servicers can demonstrate a documented, reviewable chain of custody for every EFT transaction processed through the platform.

Explore related knowledge

Access a wealth of resources to deepen your understanding of the lending industry. Our Knowledge Hub offers insights, tips, and best practices to help you navigate loan origination and servicing effectively.

Manual vs. Automated Loan Servicing: What Lenders Need to Know

The modern loan servicing landscape is complex.

Renovo’s CEO Kevin Werner Shares His Perspective on Scaling Loan Operations

In this short 3-minute video, Kevin Werner, CEO of Renovo Financial, shares insights from

Explore TMO’s New Construction Draw Manager

Streamline Construction Lending with One Connected Draw Workflow Construction Draw Manager

Ready to power your business with The Mortgage Office?

Let us show you how efficient and accurate your loan management platform can be.