“We have had The Mortgage Office since 2010. It has everything we needed and what we were looking for.”

Adjustable-Rate Mortgages (ARM)

Service ARM loans with accuracy and confidence.

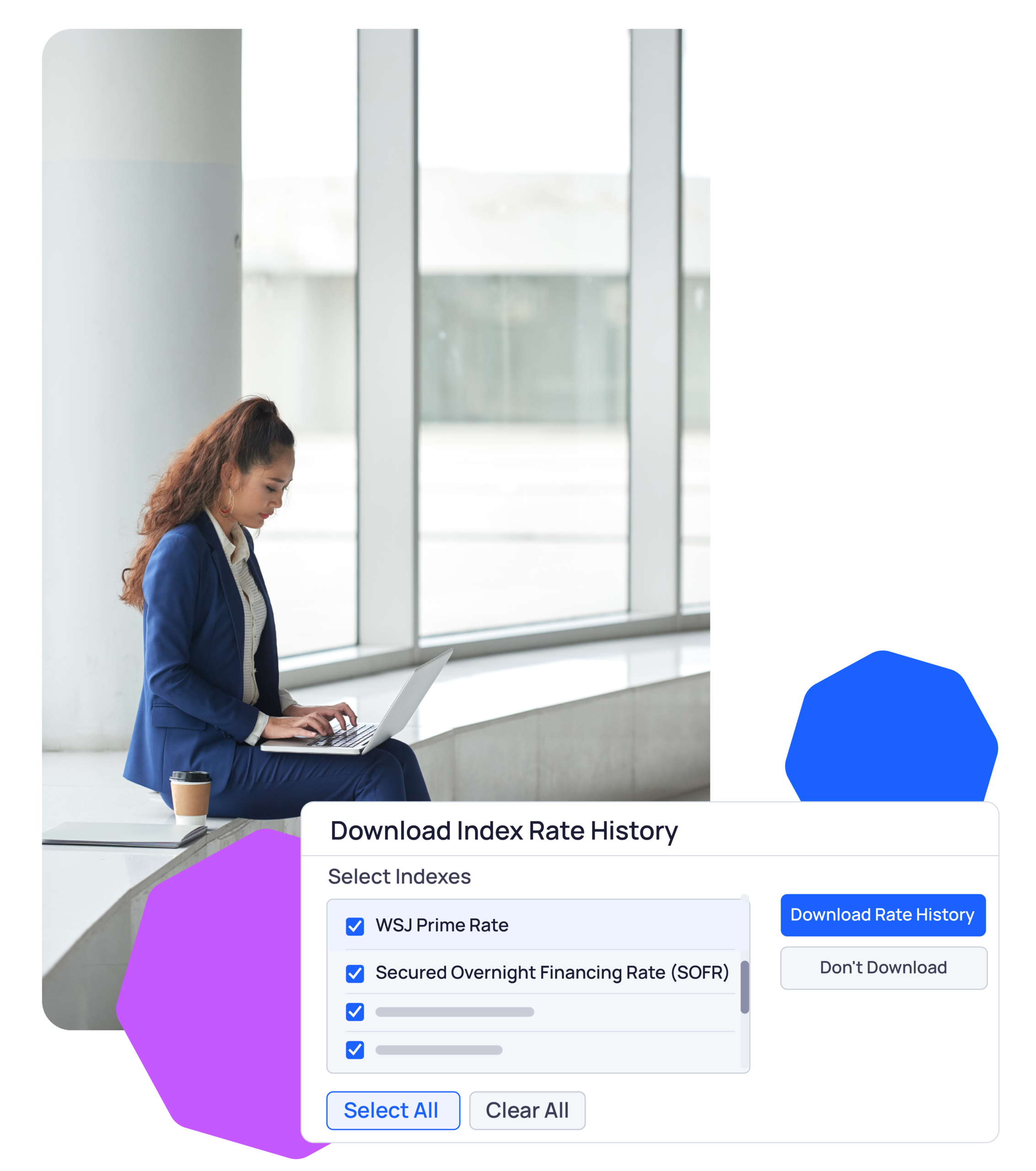

Support multiple indices across portfolios by downloading the rates and applying them to loans while adhering to granular application terms.

JUMP TO:

SEE THE DIFFERENCE

Take control of ARM servicing.

Servicing adjustable-rate loans no longer requires manual rate calculations and disclosure deadlines tracked across spreadsheets and calendars. With TMO, you can apply rate adjustments accurately, deliver compliant notices on schedule, and stay audit-ready without added complexity.

- Calculate rate adjustments accurately from the right index and margin

- Deliver borrower notices within required regulatory timeframes

- Maintain clean, compliant, audit-ready records

Solutions & Capabilities

Simplify the moving pieces when servicing Adjustable-Rate Loans.

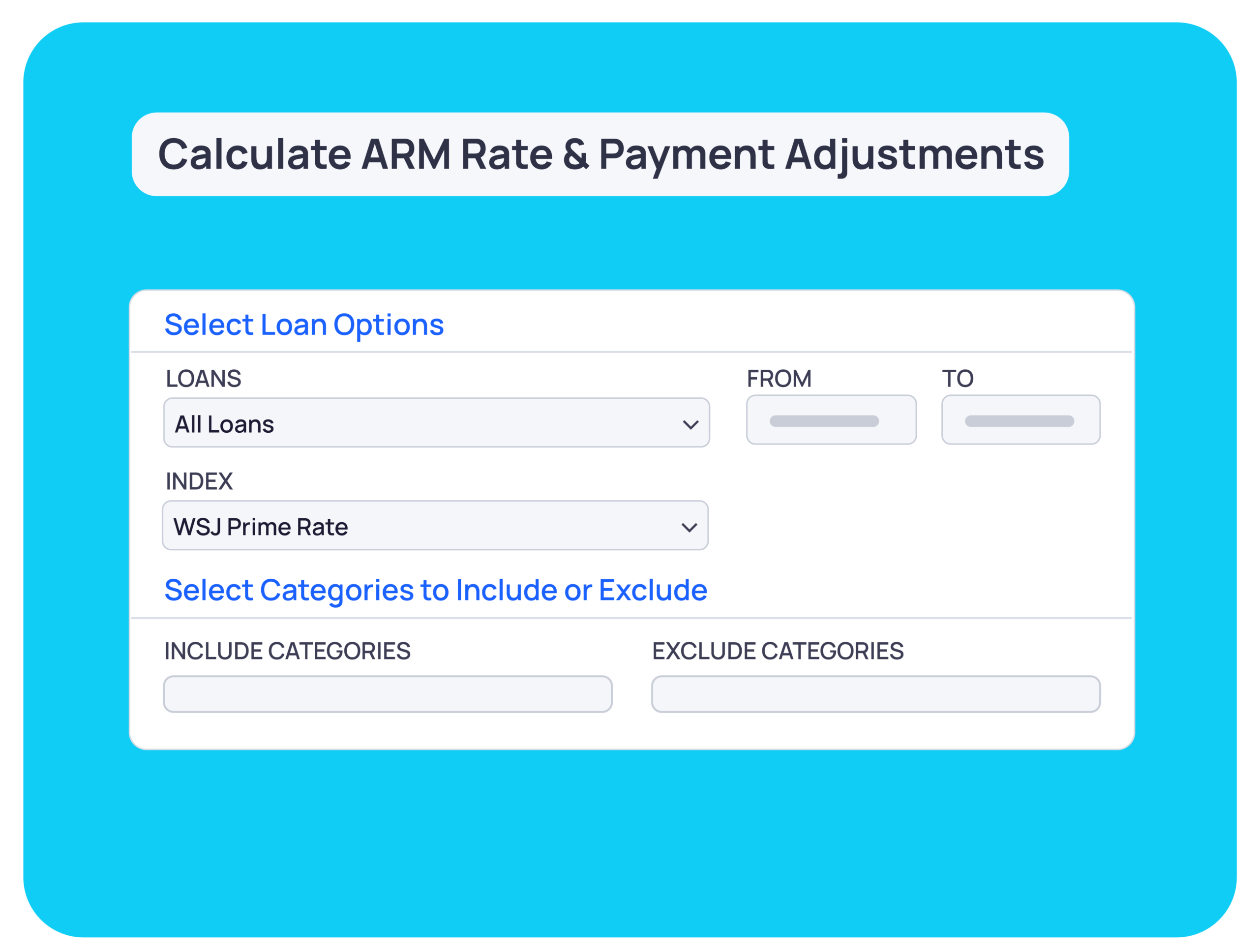

Rate Adjustment Management

Apply interest rate changes exactly as defined in each loan’s note, using the correct index, margin, and adjustment terms. Built with native support for over 50 indices.

- Tie each loan to its contractual index, margin, and rate caps

- Apply periodic and lifetime caps and floors automatically

- Recalculate payment amounts and escrow with every adjustment

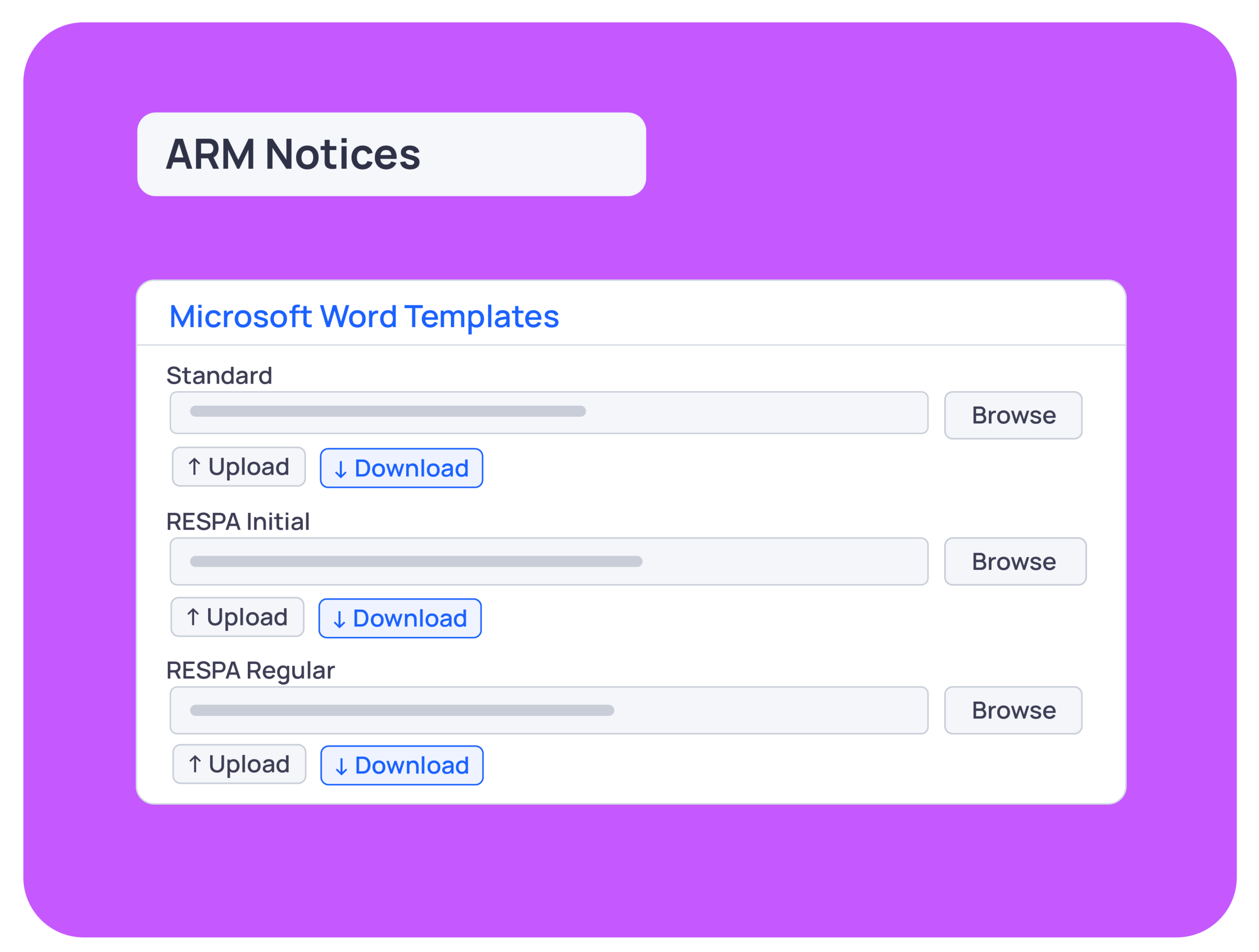

Compliance Notices & Disclosures

Generate and deliver rate adjustment notices that meet Regulation Z timing and content requirements for every covered loan.

- Track initial notice windows before the first adjusted payment

- Track subsequent notice windows before each change

- Include required content: rate comparison, payment changes, and adjustment limits

Reporting & Audit Readiness

Every rate change, notice, and calculation is retained for readily available reporting with just a few clicks.

- Audit trails for every adjustment and disclosure

- Prebuilt servicing and compliance reports

- Open API for further data extraction

HOW IT WORKS

ARM servicing made simple.

Step 1

Configure loan terms

Set each loan’s index, margin, caps, floors, and adjustment schedule so every rate change follows the note.

Step 2

Calculate adjustments

Apply the correct index value at each change date to recalculate the rate and payment accurately.

Step 3

Deliver notices

Generate compliant rate adjustment notices and send them within required regulatory timeframes.

Step 4

Stay audit-ready

Retain complete records of every adjustment and disclosure to support compliance and make audits faster and easier.

See ARM servicing in action.

SECURITY & COMPLIANCE

Keep ARM servicing compliant and audit-ready.

Maintain control over rate adjustments with clear visibility, structured workflows, and built-in safeguards that support accurate calculations and timely, compliant disclosures

- Apply rate changes with clear, auditable records

- Maintain compliance with structured controls and timing alerts

- Support audit readiness with complete, organized documentation

Partnerships & Integrations

Connect ARM servicing and our robust servicing platform with your team’s existing tools and other powerful integrations to keep rate data consistent, reduce manual work, and strengthen reporting as you scale.

FAQs

What is ARM loan servicing?

ARM loan servicing is the ongoing management of adjustable-rate mortgages, including calculating interest rate changes, recalculating payments and escrow, and delivering required disclosures to borrowers as the rate adjusts over the life of the loan. Each adjustment must follow the loan’s contractual terms and meet federal disclosure requirements to remain compliant. The Mortgage Office automates these adjustments and disclosures so servicers can manage adjustable-rate loans accurately at any volume.

What compliance requirements apply to servicing ARM loans?

ARM servicing is governed primarily by the Truth in Lending Act and its implementing Regulation Z, which set when and how servicers must disclose upcoming rate and payment changes to borrowers. Servicers must also follow the loan’s note terms for index selection and rate calculation, and meet escrow requirements under RESPA’s Regulation X. The Mortgage Office is built to apply these rules consistently, reducing the manual tracking that leads to violations.

When must a servicer send an ARM rate adjustment notice?

Under Regulation Z, the first time an ARM’s rate changes in a way that affects the payment, the servicer must send notice at least 210 days but no more than 240 days before the first payment at the new rate. For each subsequent rate change, the notice window is 60 to 120 days before the first adjusted payment. The Mortgage Office tracks these timing windows for every covered loan so notices go out within the required period.

How is an ARM interest rate calculated at each adjustment?

An ARM rate is calculated by adding the loan’s contractual margin to the current value of its index, then applying any periodic or lifetime caps and floors defined in the note. Using the wrong index value or misapplying a cap is a common source of miscalculated rates and audit findings. The Mortgage Office ties each loan to its correct index and adjustment terms so rates are calculated accurately every time.

Why do ARM servicing errors often come from manual processes?

Many ARM calculation errors trace back to manual data entry, where an incorrect index value, margin, or cap is entered into the servicing system and produces a wrong rate or payment. Because adjustments compound over the life of a loan, a single input error can create lasting discrepancies. The Mortgage Office reduces this risk by applying contractual terms automatically rather than relying on manual recalculation.

What records should a servicer keep for ARM compliance?

Servicers should retain a complete record of each rate change, including the index value used, the calculation applied, the resulting rate and payment, and a copy of every disclosure sent with its delivery date. These records let examiners verify that adjustments matched the note and that notices met timing and content rules. The Mortgage Office stores this history within each loan so documentation is available on demand.

What’s the difference between initial and subsequent ARM rate change notices?

The initial rate change notice applies the first time an ARM adjusts and carries a longer lead time of 210 to 240 days before the first adjusted payment, while subsequent notices apply to later changes with a shorter 60 to 120 day window. The required content also differs slightly between the two. The Mortgage Office distinguishes between initial and subsequent adjustments automatically so the right notice goes out at the right time.

What questions should I ask when evaluating ARM servicing software?

Ask whether the system ties each loan to its contractual index, margin, and caps, whether it tracks both initial and subsequent notice windows automatically, and whether it generates disclosures with the content Regulation Z requires. Also confirm whether rate change history and notice records are retained within the platform for audits. Requesting a live demo that walks through a rate adjustment and the resulting notice is the most reliable way to assess whether a platform meets your operational requirements.

How does automated ARM servicing reduce compliance risk?

Automated ARM servicing reduces risk by applying contractual terms consistently, calculating each adjustment from the correct index and caps, and surfacing notice deadlines before they pass. This removes the manual steps where rate errors and missed disclosures typically originate. The Mortgage Office provides this control at the loan level so servicing teams maintain accuracy and compliance as their adjustable-rate portfolio grows.

Explore related knowledge

Access a wealth of resources to deepen your understanding of the lending industry. Our Knowledge Hub offers insights, tips, and best practices to help you navigate loan origination and servicing effectively.

Manual vs. Automated Loan Servicing: What Lenders Need to Know

The modern loan servicing landscape is complex.

Renovo’s CEO Kevin Werner Shares His Perspective on Scaling Loan Operations

In this short 3-minute video, Kevin Werner, CEO of Renovo Financial, shares insights from

7 Ways to Modernize Your Loan Programs: The TMO Playbook

Learn the strategies already trusted by more than 25 counties and a growing number of hous

Ready to power your business with The Mortgage Office?

Let us show you how efficient and accurate your loan management platform can be.